Guides

LLC vs. Corporation: Which Is Right for Your Business?

Choosing between an LLC and a corporation affects taxes, paperwork, ownership rules, and how you run the business day to day. This guide gives general educational information, not legal advice, and can help you spot when it makes sense to check your state’s Secretary of State website, IRS.gov, or talk with a licensed attorney.

Start with the basic terms

LLC means limited liability company. It is a legal business structure created under state law that can help separate the owner’s personal assets from business debts and claims.

A corporation is also a separate legal business structure created under state law. It usually has more formal rules for ownership, management, recordkeeping, and decision-making.

An S-corp means an S corporation tax election. It is not a separate business structure by itself. It is a federal tax status that some eligible LLCs and corporations can choose with the IRS.

A C-corp means a C corporation for federal tax purposes. This is the default tax treatment for most corporations unless they properly elect S-corp status.

An EIN means Employer Identification Number. It is the business tax ID issued by the IRS and is often needed for hiring, banking, and tax filings.

A registered agent is the person or company listed with the state to receive legal and government documents for the business.

An operating agreement is the main internal document for an LLC. It explains who owns the LLC, how decisions are made, how profits are shared, and what happens if an owner leaves.

Articles of organization are the formation document usually filed with a state to create an LLC.

A DBA means doing business as. It is a filed business name used by a company that is different from its legal name.

If you are still deciding what structure fits best, how to form an LLC in the US and what is an EIN and how to get one are good next reads.

How LLCs and corporations are similar

Both LLCs and corporations can help create a legal separation between the business and the owner. In practice, that can reduce personal exposure if the business is sued or cannot pay a debt, but the protection is not automatic or unlimited. Owners still need to follow the law, keep business and personal finances separate, sign contracts correctly, and maintain the entity properly.

Both structures usually require:

- a state formation filing

- a registered agent

- an EIN in many real-world situations

- ongoing state filings or reports

- business licenses or permits depending on the industry and city

- separate tax and accounting records

For both types, the exact rules depend on the state where you form and operate the business. Always confirm filing rules and annual requirements with the Secretary of State and tax details with IRS.gov.

If you want help comparing formation and compliance tasks, see business entity formation and business compliance and licensing.

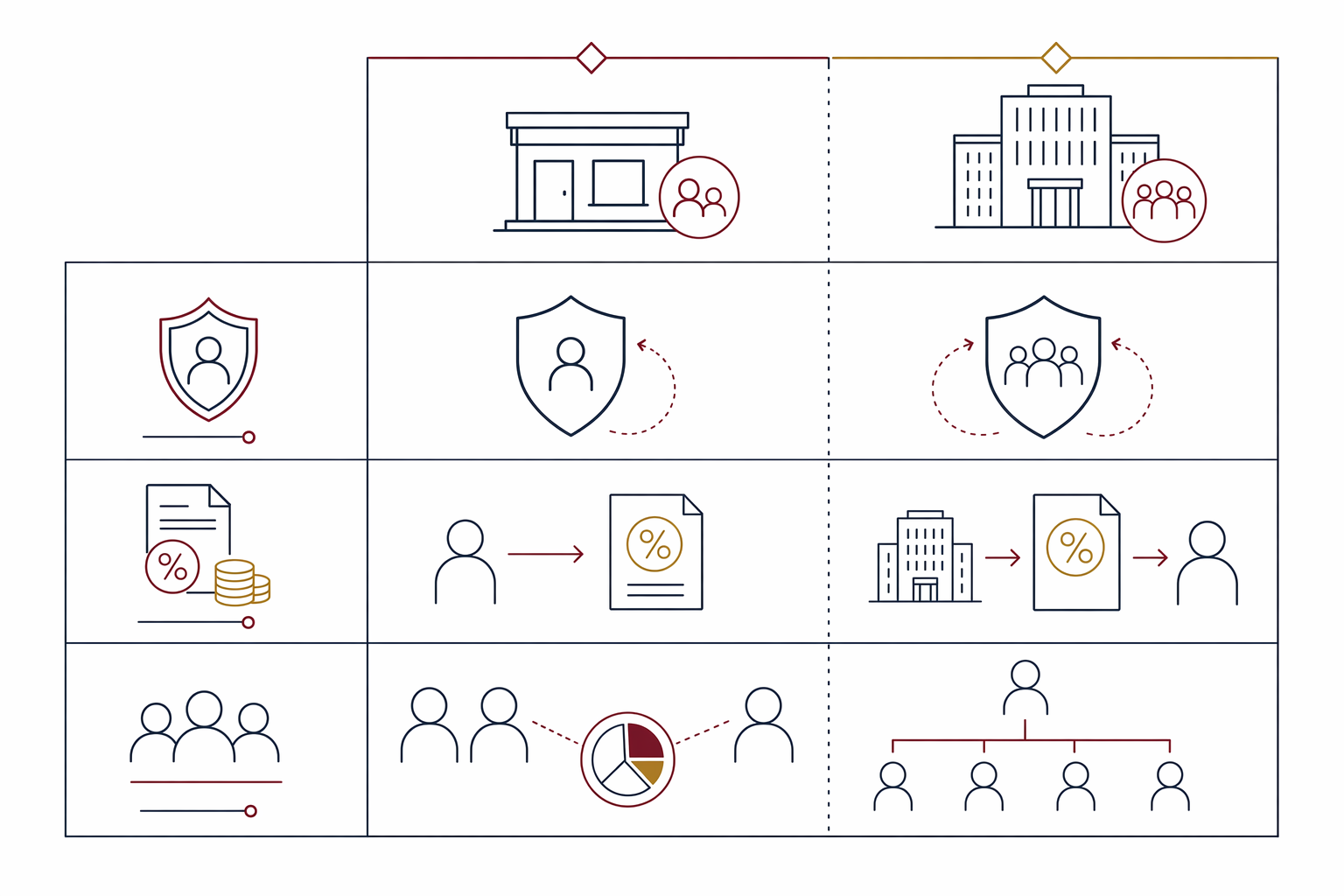

The main differences: taxes, ownership, and paperwork

For many small businesses, the biggest differences are taxes, ownership flexibility, and how formal the company needs to be.

Taxes

An LLC is often simpler at the start. A one-owner LLC is usually taxed by default like a sole proprietorship for federal tax purposes, and a multi-owner LLC is usually taxed like a partnership, unless it elects corporate tax treatment. That means profits may pass through to the owners’ personal tax returns.

A corporation is usually taxed as a C-corp by default. A C-corp pays corporate income tax, and then shareholders may also pay tax on dividends they receive. People often call this "double taxation."

An eligible LLC or corporation may elect S-corp tax treatment with the IRS. This can reduce self-employment tax in some situations, but it also adds payroll and compliance requirements. S-corp eligibility has strict limits, including rules about shareholders and stock structure. IRS.gov is the official source for those rules.

Ownership

LLCs are usually more flexible. They can be a good fit for a solo owner, a married couple, friends starting a service business, or a family-owned company that wants custom rules in the operating agreement.

Corporations are often better suited for businesses planning to issue stock, bring in multiple investors, set up formal governance, or grow in a way that requires clearer ownership rules. Venture capital investors often prefer corporations, especially Delaware corporations, but not every startup needs that.

Paperwork and formalities

LLCs generally have fewer required formalities. They still need good records, but in many states they do not have to hold the same formal annual meetings or keep the same types of corporate minutes as corporations.

Corporations usually require more formal governance. That often includes directors, officers, bylaws, stock records, board actions, and shareholder actions. These steps are manageable, but they do require discipline.

If you are unsure whether tax planning is driving the choice, it may help to speak with both a CPA and a licensed attorney. FoundryCounsel is not a law firm and does not provide legal advice, but you can get matched with a licensed business attorney for a free connection.

When an LLC may make more sense

An LLC is often the practical choice when the business needs liability separation without a lot of corporate formalities.

Common examples:

- a freelance designer or consultant with one owner

- a small online store run by one or two founders

- a local service business such as cleaning, catering, landscaping, or repair work

- a family business that wants flexible profit-sharing rules

- a business that wants the option to start simple and later review whether an S-corp tax election makes sense

An LLC may be a better fit if you want:

- simpler management rules

- fewer formal meeting requirements

- flexibility in how profits and responsibilities are allocated, subject to law and tax rules

- a structure many banks, vendors, and landlords are familiar with

But LLCs are not always simple in every state. Some states charge annual fees, franchise taxes, publication fees, or reporting fees. State filing and maintenance costs are state-dependent and commonly range from about $50 to $800 or more for formation and recurring filings, depending on the state and the business. These ranges are not quotes.

If you form an LLC, do not skip the operating agreement just because your state may not require you to file it. It is one of the most important documents for preventing owner disputes later. If you have co-founders, read partnership and founder agreements.

When a corporation may make more sense

A corporation may be worth the extra paperwork when the business needs a more formal ownership structure or plans to raise money from investors.

Common examples:

- a startup planning to seek outside investment

- a business that wants to issue stock to founders, employees, or investors

- a company that expects more complex governance and approval rules

- a business that may benefit from retaining earnings inside the company, depending on tax advice

A corporation may be a better fit if you want:

- a well-known stock-based ownership model

- clearer pathways for issuing shares

- a structure some investors and accelerators prefer

- formal board oversight from the beginning

Still, a corporation is not automatically the "serious business" choice for everyone. Many successful small businesses stay as LLCs for years. If you choose a corporation, be ready for more administration such as bylaws, stock issuance records, board and shareholder approvals, and ongoing corporate maintenance.

If your business will sign customer contracts, hire contractors, or lease space, the entity choice should also line up with your documents. See contracts and agreements and commercial leases and real estate.

A practical way to decide

If you are stuck, use this checklist.

- Ask how many owners there will be now and in the next 12 to 24 months.

- Ask whether you expect outside investors, stock grants, or venture capital.

- Ask whether simple operations matter more than formal governance.

- Ask whether your expected profits may justify reviewing S-corp tax treatment with a CPA.

- Ask what your state charges for formation, annual reports, franchise taxes, and other filings.

- Ask whether your co-owners need custom rules on voting, buyouts, deadlocks, or profit splits.

- Ask whether your bank, landlord, or major client has entity-type requirements.

A simple rule of thumb:

- If you are a small owner-operated business and want flexibility, start by examining an LLC.

- If you plan to issue stock, raise institutional money, or build a formal investor-ready structure, examine a corporation.

- If taxes are the main reason you are deciding, do not guess. Review the facts with a CPA and a licensed attorney.

You can also compare setup steps in how to form an LLC in the US and learn more about the process at how it works.

What to file, what to avoid, and when to get help

Whichever structure you choose, use official sources.

- Check your state Secretary of State website for formation forms, naming rules, annual report deadlines, and registered agent requirements.

- Check IRS.gov for EIN applications, tax classifications, and S-corp election rules.

- If your business name matters, check USPTO.gov to review federal trademark records before investing heavily in branding.

A few common mistakes to avoid:

- choosing an entity based only on social media advice

- mixing personal and business money

- forming the business but skipping the operating agreement or corporate bylaws

- failing to sign contracts in the company name

- missing annual reports or franchise tax deadlines

- assuming an S-corp is a type of company instead of a tax election

You may also hear about a BOI report, which means a Beneficial Ownership Information report. It is a federal ownership reporting requirement that has changed over time and may change again. Always confirm the current rule through the official federal source and, if needed, a licensed attorney.

If you want help finding a lawyer, get matched for free. Share only your contact information and a short description of what you need. Do not send Social Security numbers, tax ID numbers, bank details, immigration status, or confidential business secrets through a form.

For broader help on business law topics, visit guides, services, or help.

An honest note

This is general educational information, not legal advice, and does not create an attorney-client relationship. Laws and fees vary by state and change over time — confirm details with a licensed attorney and official sources before you act.

If you want a simpler structure, an LLC is often the first thing to examine, but if you want stock, investors, or more formal governance, a corporation may fit better.

Common questions

Is an LLC better than a corporation for a small business?

Sometimes, but not always. An LLC is often simpler and more flexible for owner-operated businesses, while a corporation may fit better if you plan to issue stock or raise outside investment.

Is an S-corp the same as an LLC?

No. An LLC is a legal structure formed under state law, while an S-corp is a federal tax election that some eligible LLCs and corporations can choose.

Can I change from an LLC to a corporation later?

Often yes, but the process depends on state law, tax issues, contracts, and ownership details. A conversion can trigger filing, tax, and document questions, so it is smart to review the plan with a licensed attorney and a CPA.

How much does it cost to form an LLC or corporation?

Costs vary by state and sometimes by publication, annual report, and franchise tax rules. State-dependent formation and maintenance costs commonly range from about $50 to $800 or more, and those ranges are not quotes.

Do I need an attorney to choose between an LLC and a corporation?

Not always, but legal help is useful when there are co-founders, investors, custom ownership terms, licensing issues, or plans to raise money. FoundryCounsel is not a law firm and does not give legal advice, but it can help you connect with a licensed attorney.

Ready to talk to a business-law attorney?

Get matched, free, with licensed business attorneys in your state. You compare flat-fee quotes and choose who to hire — and you confirm the fee and scope in writing before any work starts.